SOUTH TEXAS REGIONAL REPORT

Research

All Standard Disclaimers Apply & Seller Rights Retained

EAGLE FORD & AUSTIN CHALK

July 17, 2023 Study. 40-Pages

EAGLE FORD & AUSTIN CHALK

Some Conventional Comments

50-55 Rigs Running In The Play

340-Permits Issued Last 6 Mns

520-DUCs Pending

Gross Production: 2.3 MMBoepd

Covers M&A, E&P, Capital, Operations

RECORD M&A ACTIVITY IN EAGLE FORD

DOWNLOAD 40 PAGE REPORT

STUDY 1001MA

Energy Advisors has prepared a review of the Eagle Ford Area as part of our Market Monitor Series and thought leadership efforts. This 40-page Special Report provides unique perspectives on M&A, E&P and Capital Markets activity in the play.

Observations & Takeaways---

- Eagle Ford area totaled 20% of the U.S. A&D market in 1H 2023 compared to 7% historically

- EOG, Conoco and Marathon are the top producers with room for further consolidation

- In last 6 months, the sum of 587 new wells IP30 TIL reached 629,000 boepd

- The southern Austin Chalk Dorado gas play drove overall growth of the Eagle Ford area

- Murphy refracs in Karnes impressive at 10x increase and exceed original rates

- Devon and Conoco also reported improving refrac economics offering hope of ongoing new development when the acreage runs out

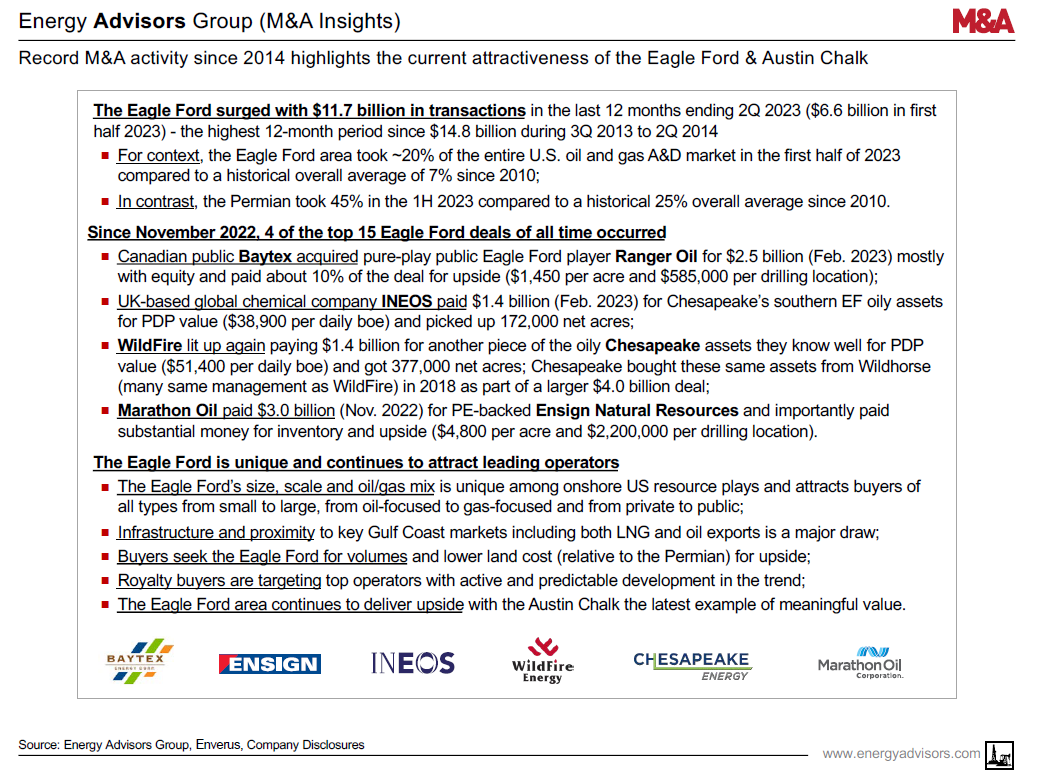

- INEOS enters the play with $1.4 billion buy; Marathon expands with $3 billion buy

- Chesapeake sells most of its oily Eagle Ford assets in 2 deals for $2.8 billion in strategic pivot to natural gas

- Pure play SilverBow expects to double its oil volumes in 2023

- Conventional drilling continues with Refugio County leading with 43 new wells in last six months

Here are some excerpts from the 40 page report.

A&D - Last 12 Months highest since 2013-2014

- Eagle Ford area M&A activity in last 12 months ending June 30, 2023 totaled $11.7 billion and is the highest 12 -month total since $14.8 billion in deals from July 2013 to June 2014 and highlights the area’s attractiveness;

- The area saw ~20% of U.S. A&D value in 1H 2023 compared to historical 7% dating back to 2010;

- The scale and spectrum across all commodities make the Eagle Ford area a unique US resource play;

- The area attracts small to large operators, oil to gas focused players and public & private funded teams;

- Eagle Ford M&A still must compete with the Permian as represented by Callon’s exit from the Eagle Ford to the Permian in a unique trade with two Carnelian backed players, Ridgemar and Percussion.

E&P - Longer Laterals, Refracs

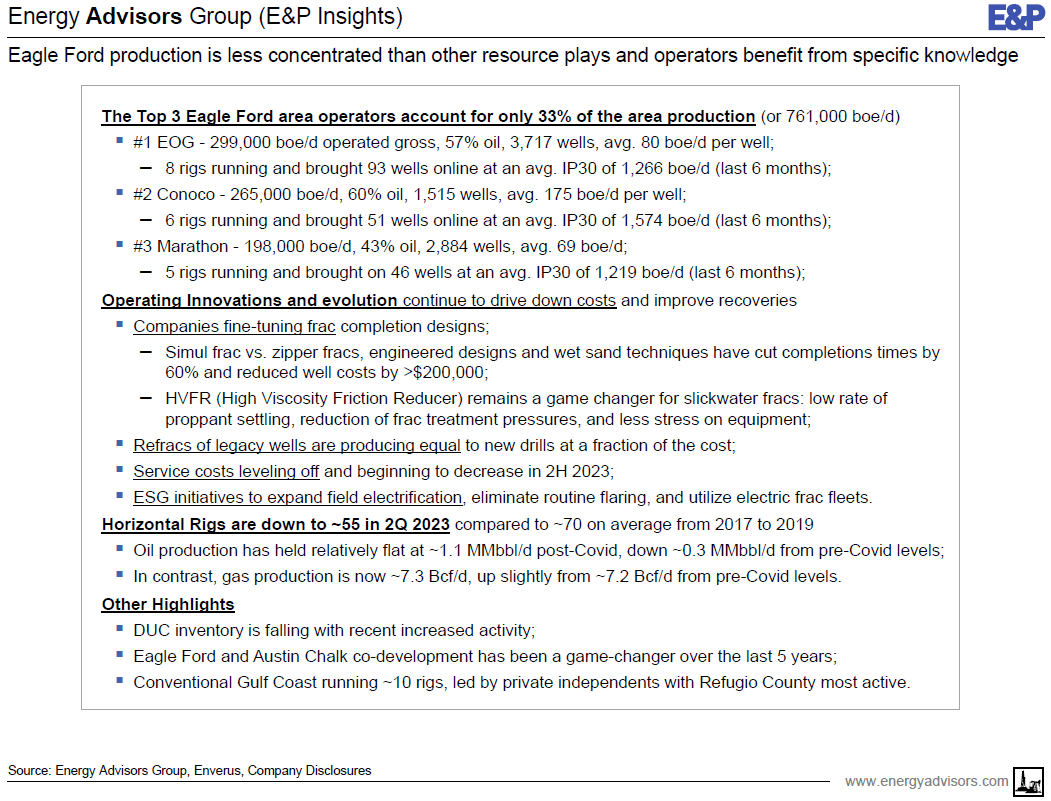

- Top 3 producers (EOG, Conoco, Marathon) account for 33% of Eagle Ford area production which leaves running room for further consolidation;

- There were 340 permits issued in last six months and ~50 horizontal rigs (~45% in Karnes and Webb Cos.) running, however the rig count is down from pre-covid rates;

- Murphy is seeing 10x production increase on (post) refracs; others seeing success as well;

- Lateral lengths have risen 30% over last 5 years while proppant loads remain stable at ~2,400 lbs/ft;

- Austin Chalk has ignited the southern portion of the Eagle Ford play as drilling in the Dorado area has surged 160% in the last two years and largely accounts for the slight overall growth of the entire Eagle Ford area;

- On the conventional side, Gulf Coast operators are currently running ~10 vertical rigs targeting the Vicksburg, Wilcox & Yegua plays.

Capital Markets - Magnolia Oil & Gas

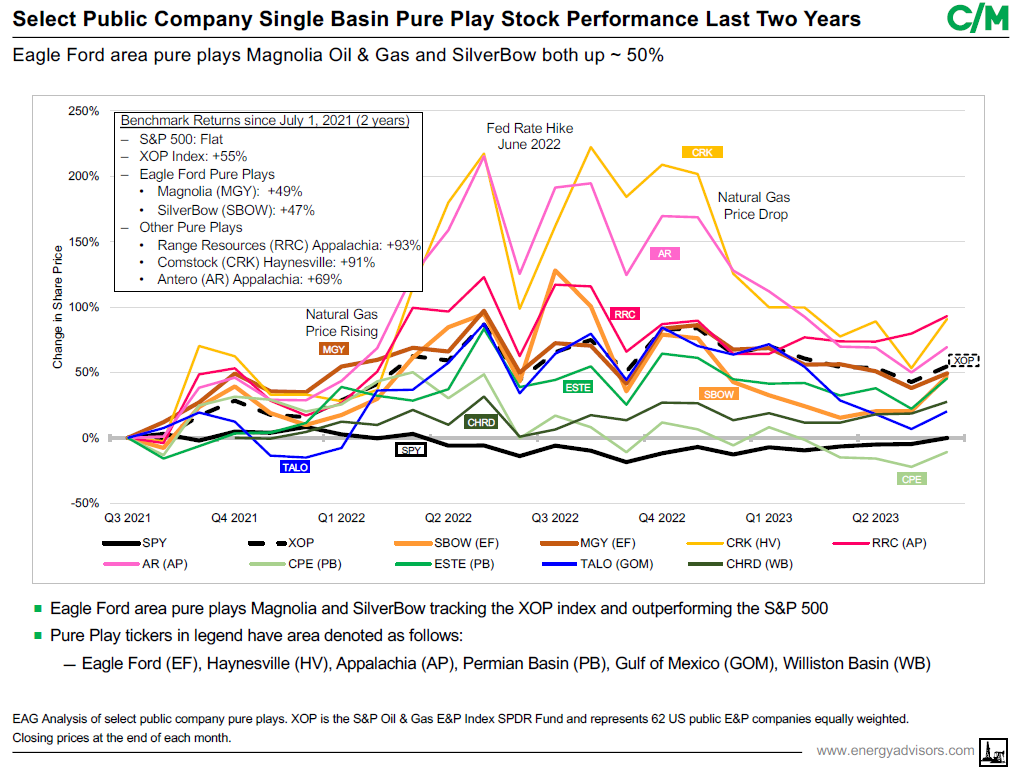

- Pure play "Eagleforder", Magnolia Oil & Gas has risen 49% in the last two years as compared to +55% for the S&P 500 Oil & Gas Index (XOP) and flat for the S&P 500;

- Large private equity players like Warburg Pincus, Kayne Anderson and Carnelian have all executed recent deals;

- Unique buyers like UK-based global chemical company INEOS’ inaugural U.S. onshore operated E&P buy for $1.4 billion bode well for the Eagle Ford area;

- The area also saw a surprise public company merger with Canada’s Baytex buying Ranger Oil for largely equity (76%) and a 7.6% premium based Ranger’s five-day volume weighted average price of Baytex.

Operational Highlights

Our firm has also put together some slides on operational insights and looked at Silverbow as a firm undergoing a thorough transformation on the back of the Eagle Ford.

- SilverBow tweaking Eagle Ford portfolio in a pivot to oil, expecting 25% growth

- Devon ramping up Eagle Ford while Murphy scoring 10x increase in vols on refracs

- EOG drills record lateral at 15,500 ft while Conoco commits to EF to replace Bakken declines long term

Energy Advisors is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE

Energy Advisors Group

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

EAGLE FORD & AUSTIN CHALK

July 17, 2023 Study. 40-Pages

EAGLE FORD & AUSTIN CHALK

Some Conventional Comments

50-55 Rigs Running In The Play

340-Permits Issued Last 6 Mns

520-DUCs Pending

Gross Production: 2.3 MMBoepd

Covers M&A, E&P, Capital, Operations

RECORD M&A ACTIVITY IN EAGLE FORD

DOWNLOAD 40 PAGE REPORT

STUDY 1001MA

Energy Advisors has prepared a review of the Eagle Ford Area as part of our Market Monitor Series and thought leadership efforts. This 40-page Special Report provides unique perspectives on M&A, E&P and Capital Markets activity in the play.

Observations & Takeaways---

- Eagle Ford area totaled 20% of the U.S. A&D market in 1H 2023 compared to 7% historically

- EOG, Conoco and Marathon are the top producers with room for further consolidation

- In last 6 months, the sum of 587 new wells IP30 TIL reached 629,000 boepd

- The southern Austin Chalk Dorado gas play drove overall growth of the Eagle Ford area

- Murphy refracs in Karnes impressive at 10x increase and exceed original rates

- Devon and Conoco also reported improving refrac economics offering hope of ongoing new development when the acreage runs out

- INEOS enters the play with $1.4 billion buy; Marathon expands with $3 billion buy

- Chesapeake sells most of its oily Eagle Ford assets in 2 deals for $2.8 billion in strategic pivot to natural gas

- Pure play SilverBow expects to double its oil volumes in 2023

- Conventional drilling continues with Refugio County leading with 43 new wells in last six months

Here are some excerpts from the 40 page report.

A&D - Last 12 Months highest since 2013-2014

- Eagle Ford area M&A activity in last 12 months ending June 30, 2023 totaled $11.7 billion and is the highest 12 -month total since $14.8 billion in deals from July 2013 to June 2014 and highlights the area’s attractiveness;

- The area saw ~20% of U.S. A&D value in 1H 2023 compared to historical 7% dating back to 2010;

- The scale and spectrum across all commodities make the Eagle Ford area a unique US resource play;

- The area attracts small to large operators, oil to gas focused players and public & private funded teams;

- Eagle Ford M&A still must compete with the Permian as represented by Callon’s exit from the Eagle Ford to the Permian in a unique trade with two Carnelian backed players, Ridgemar and Percussion.

E&P - Longer Laterals, Refracs

- Top 3 producers (EOG, Conoco, Marathon) account for 33% of Eagle Ford area production which leaves running room for further consolidation;

- There were 340 permits issued in last six months and ~50 horizontal rigs (~45% in Karnes and Webb Cos.) running, however the rig count is down from pre-covid rates;

- Murphy is seeing 10x production increase on (post) refracs; others seeing success as well;

- Lateral lengths have risen 30% over last 5 years while proppant loads remain stable at ~2,400 lbs/ft;

- Austin Chalk has ignited the southern portion of the Eagle Ford play as drilling in the Dorado area has surged 160% in the last two years and largely accounts for the slight overall growth of the entire Eagle Ford area;

- On the conventional side, Gulf Coast operators are currently running ~10 vertical rigs targeting the Vicksburg, Wilcox & Yegua plays.

Capital Markets - Magnolia Oil & Gas

- Pure play "Eagleforder", Magnolia Oil & Gas has risen 49% in the last two years as compared to +55% for the S&P 500 Oil & Gas Index (XOP) and flat for the S&P 500;

- Large private equity players like Warburg Pincus, Kayne Anderson and Carnelian have all executed recent deals;

- Unique buyers like UK-based global chemical company INEOS’ inaugural U.S. onshore operated E&P buy for $1.4 billion bode well for the Eagle Ford area;

- The area also saw a surprise public company merger with Canada’s Baytex buying Ranger Oil for largely equity (76%) and a 7.6% premium based Ranger’s five-day volume weighted average price of Baytex.

Operational Highlights

Our firm has also put together some slides on operational insights and looked at Silverbow as a firm undergoing a thorough transformation on the back of the Eagle Ford.

- SilverBow tweaking Eagle Ford portfolio in a pivot to oil, expecting 25% growth

- Devon ramping up Eagle Ford while Murphy scoring 10x increase in vols on refracs

- EOG drills record lateral at 15,500 ft while Conoco commits to EF to replace Bakken declines long term

Energy Advisors is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE

Energy Advisors Group

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123