02Q24 QUARTERLY M&A REPORT

Research

All Standard Disclaimers Apply & Seller Rights Retained

DEAL PERSPECTIVES (MEDIA VERSION)

Quick 9 Pages of The Full 39 Page Report

2Q24 DEAL VALUE SLOWS SOME

$30.6B in 2Q24 - Down from $51.2B in 1Q

22 2Q Deals - Down from 26 in 1Q

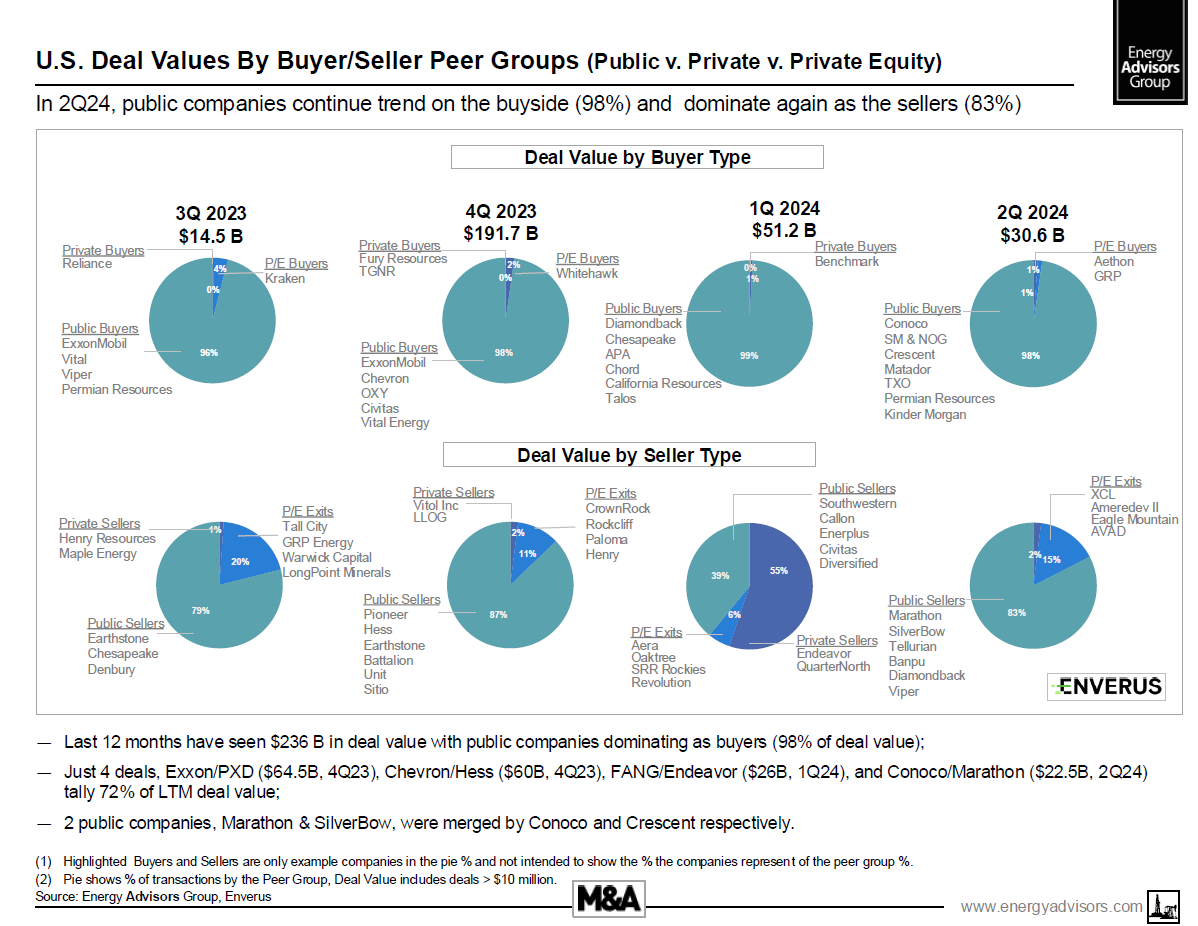

Public Companies Buy 98% of Deals

Permian Cools with <10% Vs. 52% in 2023

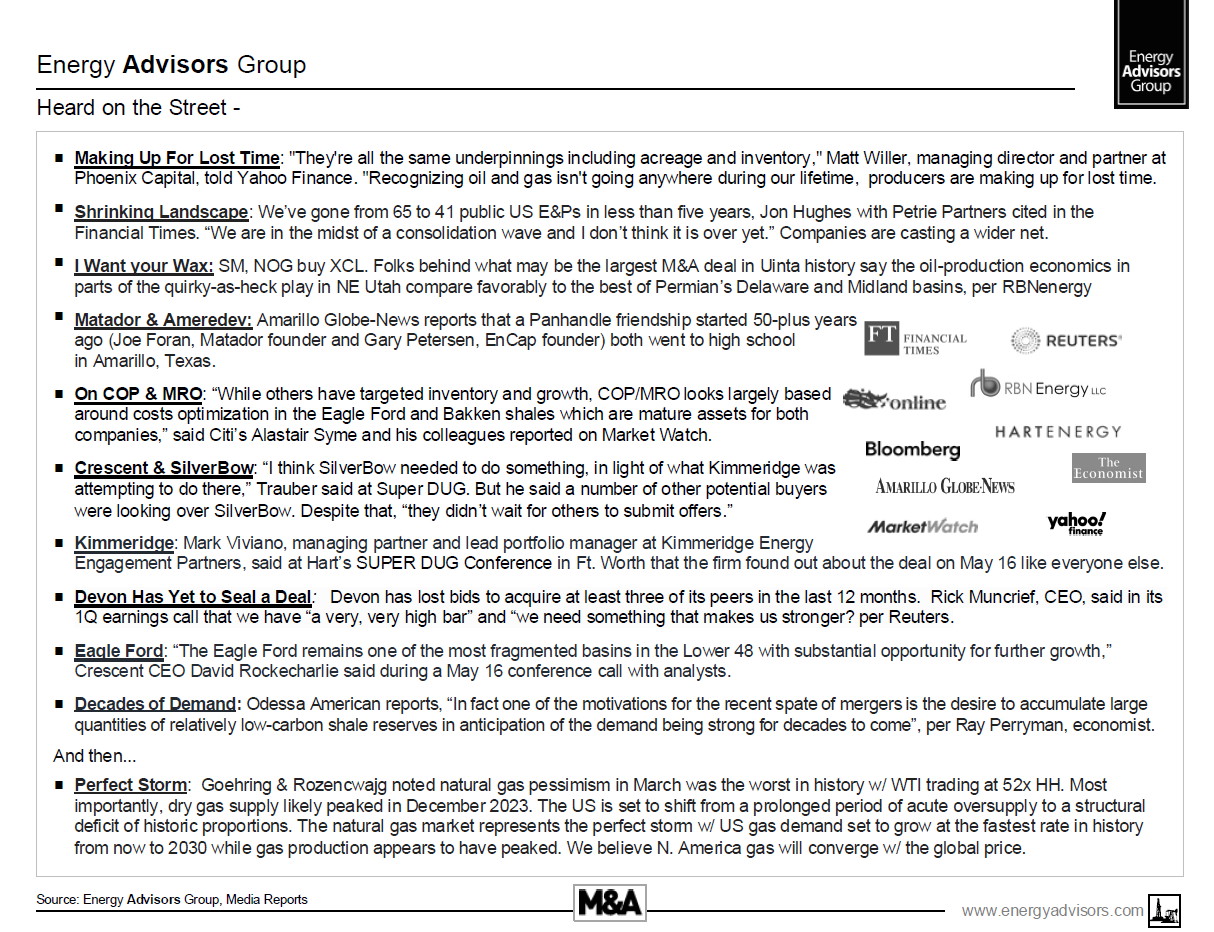

Conoco Buys Marathon for $22.5 Billion

SM + NOG Stake Ground in Uinta for $2.2B

Crescent Energy Buys SilverBow for $2.1B

Public Company Consolidation Continues

Conoco Says $2B on Chopping Block

Street Talk Still Has Devon on the Hunt

Consolidation Wave Likely Peaked

Markets Awaiting Portfolio Trimming

CONTACT EAG FOR FULL 39 PAGE REPORT

STUDY 1004MA

THIS IS THE ABBREVIATED MEDIA VERSION

Energy Advisors Group has released a Q2 2024 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. The full 39-page Special Report provides perspectives on past and current trends in deal values, counts, plays and valuations. Also included are forward looking themes as buyers and sellers look to navigate a plethora of dynamics impacting oil and gas prices, capital availability and costs, deal quality, regulatory and energy transition impacts, play economics, technology and geopolitical risks.

Energy Advisors Group has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side. Energy Advisors also provides consulting services including asset management and optimization.

Here are our quick quotes, and takeaways from our report.

Quick Quotes:

------- "How was the second quarter? Deal value slows some from $51 billion in 1Q to $31 billion in 2Q, however consolidation continuing with Conoco taking Marathon and Crescent Energy taking SilverBow – these 2 deals account for ~80% of 2Q deal value.”

------- "Oil, Oil, Oil! Oil deals take 7 of top 10 deals while owners of gas assets remain optimistic that higher prices in the short to mid term will bring significantly higher exit values and remain hesitant to sell now”.

------"Takeaway: The most striking part in 2Q 2024 is that the Permian slumped to $2.5 billion (or about 8% of

the $30.9 billion market) compared to 44% ($176.7 billion) of the $298.3 billion market since January 1, 2021.”

------“Shrinking Universe: SilverBow, formerly Swift Energy, a company founded by Earl Swift in 1979 and taken public in 1981 was one of a very few original independent public E&Ps left standing.”

------ "Tellurian Pivots - In July 2022, TELL bought an additional 45 MMcfpd for $125 MM from EnSight as a physical hedge for Driftwood – now Tellurian exits upstream strategy for cash to further fund Driftwood buildout.”

Takeaways from 2Q 2024---

- Reminder don’t be fooled. While top line remains respectable at $30.9 billion, the underlying market is slow tallying just 22 deals;

- Low natural gas prices yet healthy oil prices delivered what you would expect – oil deals transacting, gas deals still in a stall;

- Analyzing Enverus M&A data we came up w/ average production multiples of ~$43,000 ppbopd for oil & ~$3,000 ppmcfpd for natural gas;

- Enverus data shows EBITDA multiples ranging from 2.5x to 4.4x forward next twelve months EBITDA;

- On May 16, Crescent Energy surprised markets by taking SilverBow for $2.1 billion in cash and debt assumption after a long and public battle between SilverBow and Kimmeridge who chased SilverBow in an attempt to expand its Gulf Coast gas deliveries;

- Just two weeks later, Haynesville powerhouse Aethon buys Tellurian’s upstream assets as Tellurian decides it no longer needs control of supply for its Driftwood LNG facility. While large and private, Aethon signals desire to IPO to provide market a second Haynesville pure-play, besides Comstock;

- On the same day (May 29), Conoco strikes to buy Marathon in a deal for $22.5 billion in a deal driven in part by a large ReFrac opportunity on MRO’s Eagle Ford lands;

- Speaking about Conoco, the Marathon deal ($22.5B) is the third largest in corporate history, behind COP’s buy of Burlington Resources ($35.6B, Dec. 2005) and its merger with Phillips Petroleum ($23.2B, Nov. 2001) – it also follows a recent targeted campaign in the Permian where it bought Concho ($13.3B, Nov. 2020) and Shell’s Delaware Basin assets ($9.5B, Sept. 2021);

- Conoco’s divestment plans calls for selling $2B of assets across the new portfolio;

- Matador continues its acquisition spree with another buy of an EnCap company Ameredev II for $1.9 billion, as it expands its Delaware Basin focus , and comes on the heels of closing a $1.6 billion buy of EnCap backed Advance Energy. Interestingly, Matador’s Joe Foran and EnCap’s Gary Petersen trace their friendship back to mutual roots in Amarillo , Texas;

- In a twist, SM Energy and Northern Oil & Gas team up 80/20 to buy core-of-the-core Uinta waxy oil assets from XCL Resources (backed by the Rice brothers and EnCap) where SM claims strong economics and premium pricing for waxy crude due to feedstock demand for motor oil and lubricants;

- The universe of public E&P’s continues to shrink going from 65 to 41 in less than five years, per Petrie Partners;

- Word is Devon remains on the hunt although is being careful and setting a high bar for acquisition criteria so as to not get burned;

- On the heels FANG's mega merger with neighbor Endeavor, FANG sold $95 million on non-op assets during 2Q24;

- Public companies continue to dominate buyside, accounting for 98% of all deal value in U.S;

- Private equity continues to be net sellers, with EnCap & Rice Investments selling Uinta-focused XCL and EnCap also divesting Ameredev II;

- Looking ahead, we expect the ferocious pace of public company buying to slow in dollar terms and expect portfolio trimming/optimization to feed a wave of assets to the marketplace. back in 2010);

#1---

Here is additional insight from the report taken from one of our slides:

#2---

Here is some additional content:

#3---

Here is a striking slide demonstrating public companies dominating the buyside:

The 9-page media report is available to the right.

Interested parties desiring to see the whole 39 page report should email any one of us down below for the complete version.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE FULL REPORT CONTACT:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Ronyld W Wise

Founder & Managing Partner

-- Email [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

DEAL PERSPECTIVES (MEDIA VERSION)

Quick 9 Pages of The Full 39 Page Report

2Q24 DEAL VALUE SLOWS SOME

$30.6B in 2Q24 - Down from $51.2B in 1Q

22 2Q Deals - Down from 26 in 1Q

Public Companies Buy 98% of Deals

Permian Cools with <10% Vs. 52% in 2023

Conoco Buys Marathon for $22.5 Billion

SM + NOG Stake Ground in Uinta for $2.2B

Crescent Energy Buys SilverBow for $2.1B

Public Company Consolidation Continues

Conoco Says $2B on Chopping Block

Street Talk Still Has Devon on the Hunt

Consolidation Wave Likely Peaked

Markets Awaiting Portfolio Trimming

CONTACT EAG FOR FULL 39 PAGE REPORT

STUDY 1004MA

THIS IS THE ABBREVIATED MEDIA VERSION

Energy Advisors Group has released a Q2 2024 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. The full 39-page Special Report provides perspectives on past and current trends in deal values, counts, plays and valuations. Also included are forward looking themes as buyers and sellers look to navigate a plethora of dynamics impacting oil and gas prices, capital availability and costs, deal quality, regulatory and energy transition impacts, play economics, technology and geopolitical risks.

Energy Advisors Group has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side. Energy Advisors also provides consulting services including asset management and optimization.

Here are our quick quotes, and takeaways from our report.

Quick Quotes:

------- "How was the second quarter? Deal value slows some from $51 billion in 1Q to $31 billion in 2Q, however consolidation continuing with Conoco taking Marathon and Crescent Energy taking SilverBow – these 2 deals account for ~80% of 2Q deal value.”

------- "Oil, Oil, Oil! Oil deals take 7 of top 10 deals while owners of gas assets remain optimistic that higher prices in the short to mid term will bring significantly higher exit values and remain hesitant to sell now”.

------"Takeaway: The most striking part in 2Q 2024 is that the Permian slumped to $2.5 billion (or about 8% of

the $30.9 billion market) compared to 44% ($176.7 billion) of the $298.3 billion market since January 1, 2021.”

------“Shrinking Universe: SilverBow, formerly Swift Energy, a company founded by Earl Swift in 1979 and taken public in 1981 was one of a very few original independent public E&Ps left standing.”

------ "Tellurian Pivots - In July 2022, TELL bought an additional 45 MMcfpd for $125 MM from EnSight as a physical hedge for Driftwood – now Tellurian exits upstream strategy for cash to further fund Driftwood buildout.”

Takeaways from 2Q 2024---

- Reminder don’t be fooled. While top line remains respectable at $30.9 billion, the underlying market is slow tallying just 22 deals;

- Low natural gas prices yet healthy oil prices delivered what you would expect – oil deals transacting, gas deals still in a stall;

- Analyzing Enverus M&A data we came up w/ average production multiples of ~$43,000 ppbopd for oil & ~$3,000 ppmcfpd for natural gas;

- Enverus data shows EBITDA multiples ranging from 2.5x to 4.4x forward next twelve months EBITDA;

- On May 16, Crescent Energy surprised markets by taking SilverBow for $2.1 billion in cash and debt assumption after a long and public battle between SilverBow and Kimmeridge who chased SilverBow in an attempt to expand its Gulf Coast gas deliveries;

- Just two weeks later, Haynesville powerhouse Aethon buys Tellurian’s upstream assets as Tellurian decides it no longer needs control of supply for its Driftwood LNG facility. While large and private, Aethon signals desire to IPO to provide market a second Haynesville pure-play, besides Comstock;

- On the same day (May 29), Conoco strikes to buy Marathon in a deal for $22.5 billion in a deal driven in part by a large ReFrac opportunity on MRO’s Eagle Ford lands;

- Speaking about Conoco, the Marathon deal ($22.5B) is the third largest in corporate history, behind COP’s buy of Burlington Resources ($35.6B, Dec. 2005) and its merger with Phillips Petroleum ($23.2B, Nov. 2001) – it also follows a recent targeted campaign in the Permian where it bought Concho ($13.3B, Nov. 2020) and Shell’s Delaware Basin assets ($9.5B, Sept. 2021);

- Conoco’s divestment plans calls for selling $2B of assets across the new portfolio;

- Matador continues its acquisition spree with another buy of an EnCap company Ameredev II for $1.9 billion, as it expands its Delaware Basin focus , and comes on the heels of closing a $1.6 billion buy of EnCap backed Advance Energy. Interestingly, Matador’s Joe Foran and EnCap’s Gary Petersen trace their friendship back to mutual roots in Amarillo , Texas;

- In a twist, SM Energy and Northern Oil & Gas team up 80/20 to buy core-of-the-core Uinta waxy oil assets from XCL Resources (backed by the Rice brothers and EnCap) where SM claims strong economics and premium pricing for waxy crude due to feedstock demand for motor oil and lubricants;

- The universe of public E&P’s continues to shrink going from 65 to 41 in less than five years, per Petrie Partners;

- Word is Devon remains on the hunt although is being careful and setting a high bar for acquisition criteria so as to not get burned;

- On the heels FANG's mega merger with neighbor Endeavor, FANG sold $95 million on non-op assets during 2Q24;

- Public companies continue to dominate buyside, accounting for 98% of all deal value in U.S;

- Private equity continues to be net sellers, with EnCap & Rice Investments selling Uinta-focused XCL and EnCap also divesting Ameredev II;

- Looking ahead, we expect the ferocious pace of public company buying to slow in dollar terms and expect portfolio trimming/optimization to feed a wave of assets to the marketplace. back in 2010);

#1---

Here is additional insight from the report taken from one of our slides:

#2---

Here is some additional content:

#3---

Here is a striking slide demonstrating public companies dominating the buyside:

The 9-page media report is available to the right.

Interested parties desiring to see the whole 39 page report should email any one of us down below for the complete version.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE FULL REPORT CONTACT:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Ronyld W Wise

Founder & Managing Partner

-- Email [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123