03Q24 QUARTERLY M&A REPORT

Research

All Standard Disclaimers Apply & Seller Rights Retained

DEAL PERSPECTIVES (MEDIA VERSION)

Quick 9 Pages of The Full 26 Page Report

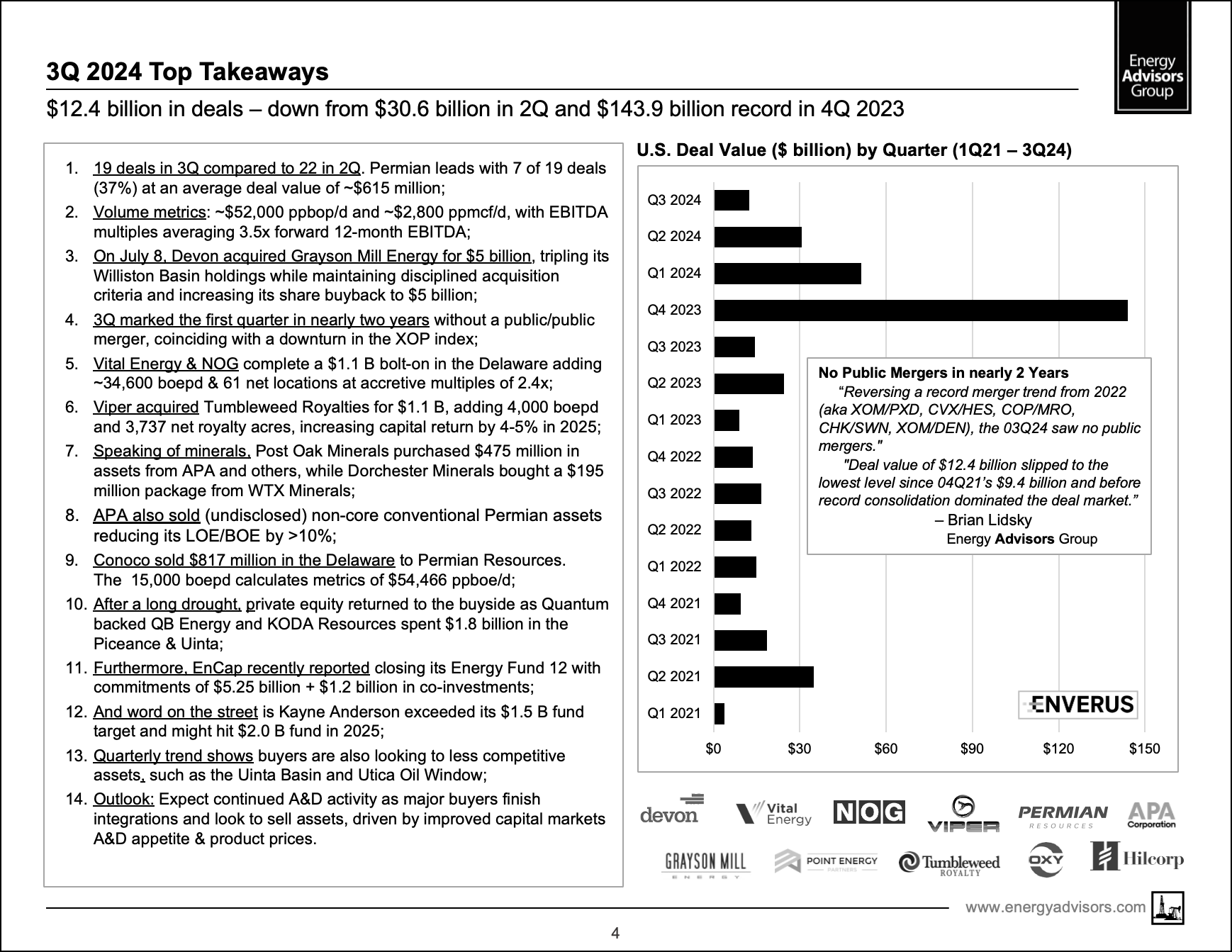

3Q24 NO PUBLIC MERGERS SINCE 2022

$12.4B in 3Q24 - Down from $30.6B in 2Q

19 3Q Deals - Down from 22 in 2Q

Private Equity Drives Top Two Deals of 3Q

Permian Still Leads with 7 of 19, or 37%

Viper Acquired Tumbleweed for $1.1 Billion

Post Oak Buys $475 MM of assets

Conventional Assets Heat Up

APA Sells non-core Permian Conventionals

Private Equity Back on the Rise

EnCap Closes Fund 12 with > $5.25 Billion

Kayne Anderson Exceeds $1.5 Billion target

Buyers Targeting Less Competitive Areas

CONTACT EAG FOR FULL 26 PAGE REPORT

STUDY 1005MA

THIS IS THE ABBREVIATED MEDIA VERSION

Energy Advisors Group has released a Q3 2024 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. The full 26-page Special Report provides perspectives on past and current trends in deal values, counts, plays and valuations. Also included are forward looking themes as buyers and sellers look to navigate a plethora of dynamics impacting oil and gas prices, capital availability and costs, deal quality, regulatory and energy transition impacts, play economics, technology and geopolitical risks.

Energy Advisors Group has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side. Energy Advisors also provides consulting services including asset management and optimization.

Here are our quick quotes, and takeaways from our report.

Quick Quotes:

------- How was the third quarter? "Deal activity in Q3 slowed slightly, dropping from $12.4 billion in Q2 to $31 billion in Q3. However, private equity dominated, with notable transactions such as Devon's $5.0 billion acquisition of Grayson Mill and the $1.8 billion sale of Caerus Oil & Gas to QB Energy & Koda Resources.”

------- Oil dominates deal flow: "Oil deals dominated the market, accounting for nine of the top ten transactions. Meanwhile, owners of gas assets remain optimistic, believing that rising prices in the short-to-medium term will lead to significantly higher exit values, causing many to hesitate on selling.”

------ Takeaway: "The most striking part in 3Q 2024 is that there were no public mergers for the first time since 4Q22.”

------Permian still leads: "The Permian Basin continues to lead in deal activity. Of the 19 transactions reported in Q3, seven—representing 37%—were in the Permian.”

------ Royalties Return - "There's been a resurgence in the mineral and royalty sector, highlighted by Viper's $1.1 billion acquisition of Tumbleweed Royalties and Post Oak's $475 million deal for APA and other assets.”

Takeaways from 3Q 2024---

- 19 deals in 3Q compared to 22 in 2Q. Permian leads with 7 of 19 deals (37%) at an average deal value of ~$615 million;

- Volume metrics: ~$52,000 ppbopd & ~$2,800 ppmcfd, with EBITDA multiples averaging 3.5x forward 12-month EBITDA;

- On July 8, Devon acquired Grayson Mill Energy for $5 billion, tripling its Williston Basin holdings while maintaining disciplined acquisition criteria and increasing its share buyback to $5 billion;

- 3Q marked the 1st quarter in nearly two years without a public/public merger, coinciding with a downturn in the XOP index;

- Vital Energy & NOG complete a $1.1 B bolt-on in the Delaware adding ~34,600 boepd & 61 net locations at accretive multiples of 2.4x;

- Viper acquired Tumbleweed Royalties for $1.1 B, adding 4,000 boepd and 3,737 net royalty acres, increasing capital return by 4-5% in 2025;

- Speaking of minerals, Post Oak Minerals purchased $475 million in assets from APA and others, while Dorchester Minerals bought a $195 million package from WTX Minerals;

- APA also sold (undisclosed) non-core conventional Permian assets reducing its LOE/BOE by >10%;

- Conoco sold $817 MM in the Delaware to Permian Resources. The 15,000 boepd calculates metrics of $54,466 ppboe/d;

- After a long drought, private equity returned to the buyside as Quantum backed QB Energy and KODA Resources spent $1.8 billion in the Piceance & Uinta;

- Furthermore, EnCap recently reported closing its Energy Fund 12 with commitments of $5.25 billion + $1.2 billion in co-investments;

- And word on the street is Kayne Anderson exceeded its $1.5 B fund target and might hit $2.0 B fund in 2025;

- Quarterly trend shows buyers are also looking to less competitive assets, such as the Uinta Basin and Utica Oil Window;

- Outlook: Expect continued A&D activity as major buyers finish integrations and look to sell assets, driven by improved market conditions and product prices.

#1---

Here is additional insight from the report taken from one of our slides:

#2---

Here is some additional content:

#3---

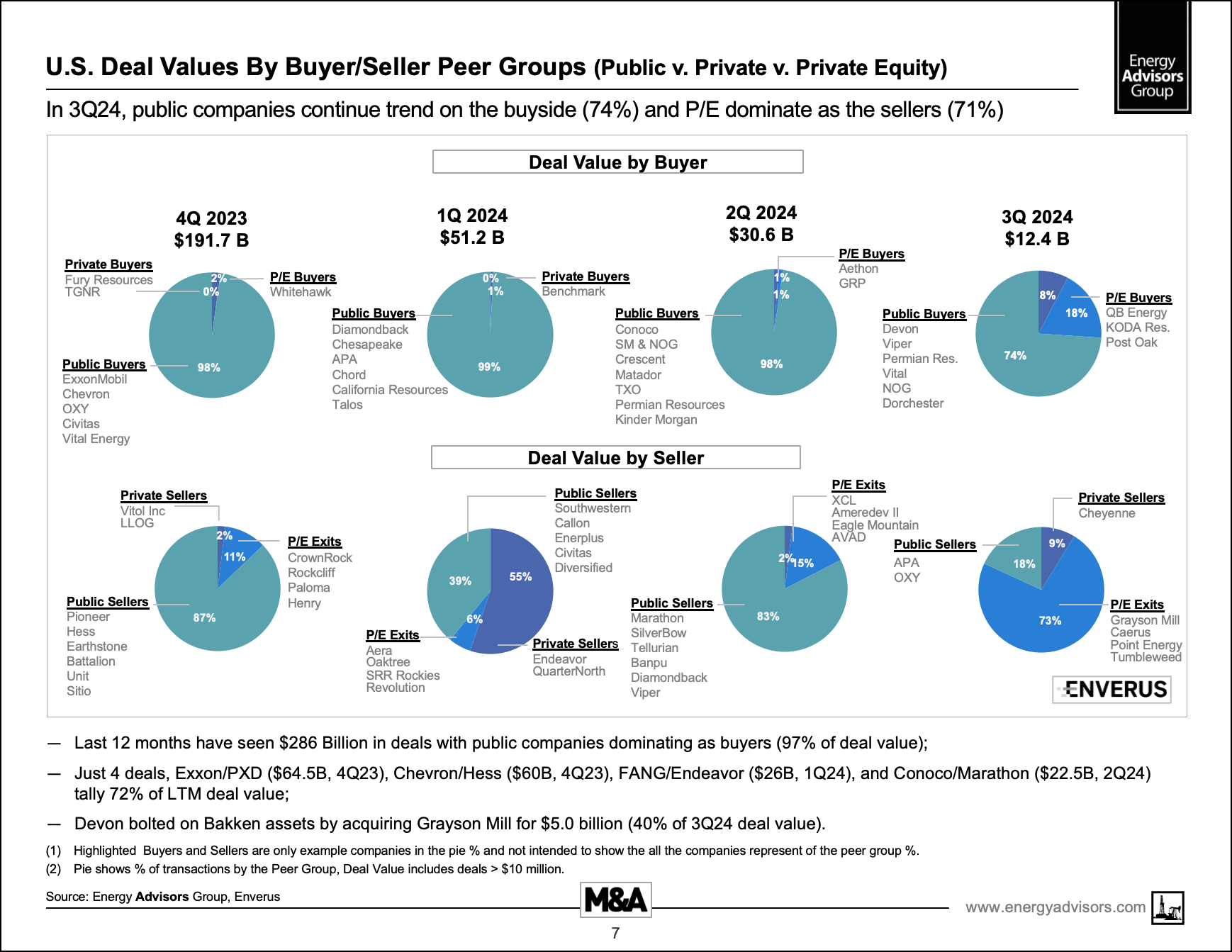

Here is a striking slide demonstrating public companies dominating the buyside:

The 9-page media report is available to the right.

Interested parties desiring to see the whole 26 page report should email any one of us down below for the complete version.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE FULL REPORT CONTACT:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Ronyld W Wise

Founder & Managing Partner

-- Email [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

DEAL PERSPECTIVES (MEDIA VERSION)

Quick 9 Pages of The Full 26 Page Report

3Q24 NO PUBLIC MERGERS SINCE 2022

$12.4B in 3Q24 - Down from $30.6B in 2Q

19 3Q Deals - Down from 22 in 2Q

Private Equity Drives Top Two Deals of 3Q

Permian Still Leads with 7 of 19, or 37%

Viper Acquired Tumbleweed for $1.1 Billion

Post Oak Buys $475 MM of assets

Conventional Assets Heat Up

APA Sells non-core Permian Conventionals

Private Equity Back on the Rise

EnCap Closes Fund 12 with > $5.25 Billion

Kayne Anderson Exceeds $1.5 Billion target

Buyers Targeting Less Competitive Areas

CONTACT EAG FOR FULL 26 PAGE REPORT

STUDY 1005MA

THIS IS THE ABBREVIATED MEDIA VERSION

Energy Advisors Group has released a Q3 2024 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. The full 26-page Special Report provides perspectives on past and current trends in deal values, counts, plays and valuations. Also included are forward looking themes as buyers and sellers look to navigate a plethora of dynamics impacting oil and gas prices, capital availability and costs, deal quality, regulatory and energy transition impacts, play economics, technology and geopolitical risks.

Energy Advisors Group has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side. Energy Advisors also provides consulting services including asset management and optimization.

Here are our quick quotes, and takeaways from our report.

Quick Quotes:

------- How was the third quarter? "Deal activity in Q3 slowed slightly, dropping from $12.4 billion in Q2 to $31 billion in Q3. However, private equity dominated, with notable transactions such as Devon's $5.0 billion acquisition of Grayson Mill and the $1.8 billion sale of Caerus Oil & Gas to QB Energy & Koda Resources.”

------- Oil dominates deal flow: "Oil deals dominated the market, accounting for nine of the top ten transactions. Meanwhile, owners of gas assets remain optimistic, believing that rising prices in the short-to-medium term will lead to significantly higher exit values, causing many to hesitate on selling.”

------ Takeaway: "The most striking part in 3Q 2024 is that there were no public mergers for the first time since 4Q22.”

------Permian still leads: "The Permian Basin continues to lead in deal activity. Of the 19 transactions reported in Q3, seven—representing 37%—were in the Permian.”

------ Royalties Return - "There's been a resurgence in the mineral and royalty sector, highlighted by Viper's $1.1 billion acquisition of Tumbleweed Royalties and Post Oak's $475 million deal for APA and other assets.”

Takeaways from 3Q 2024---

- 19 deals in 3Q compared to 22 in 2Q. Permian leads with 7 of 19 deals (37%) at an average deal value of ~$615 million;

- Volume metrics: ~$52,000 ppbopd & ~$2,800 ppmcfd, with EBITDA multiples averaging 3.5x forward 12-month EBITDA;

- On July 8, Devon acquired Grayson Mill Energy for $5 billion, tripling its Williston Basin holdings while maintaining disciplined acquisition criteria and increasing its share buyback to $5 billion;

- 3Q marked the 1st quarter in nearly two years without a public/public merger, coinciding with a downturn in the XOP index;

- Vital Energy & NOG complete a $1.1 B bolt-on in the Delaware adding ~34,600 boepd & 61 net locations at accretive multiples of 2.4x;

- Viper acquired Tumbleweed Royalties for $1.1 B, adding 4,000 boepd and 3,737 net royalty acres, increasing capital return by 4-5% in 2025;

- Speaking of minerals, Post Oak Minerals purchased $475 million in assets from APA and others, while Dorchester Minerals bought a $195 million package from WTX Minerals;

- APA also sold (undisclosed) non-core conventional Permian assets reducing its LOE/BOE by >10%;

- Conoco sold $817 MM in the Delaware to Permian Resources. The 15,000 boepd calculates metrics of $54,466 ppboe/d;

- After a long drought, private equity returned to the buyside as Quantum backed QB Energy and KODA Resources spent $1.8 billion in the Piceance & Uinta;

- Furthermore, EnCap recently reported closing its Energy Fund 12 with commitments of $5.25 billion + $1.2 billion in co-investments;

- And word on the street is Kayne Anderson exceeded its $1.5 B fund target and might hit $2.0 B fund in 2025;

- Quarterly trend shows buyers are also looking to less competitive assets, such as the Uinta Basin and Utica Oil Window;

- Outlook: Expect continued A&D activity as major buyers finish integrations and look to sell assets, driven by improved market conditions and product prices.

#1---

Here is additional insight from the report taken from one of our slides:

#2---

Here is some additional content:

#3---

Here is a striking slide demonstrating public companies dominating the buyside:

The 9-page media report is available to the right.

Interested parties desiring to see the whole 26 page report should email any one of us down below for the complete version.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE FULL REPORT CONTACT:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Ronyld W Wise

Founder & Managing Partner

-- Email [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123