PERMIAN (DB) REGIONAL STUDY

Research

All Standard Disclaimers Apply & Seller Rights Retained

REGIONAL STUDY - Energy Advisors Group")

DELAWARE BASIN PERSPECTIVES

August 2, 2023; 42-Page Report

Delaware Basin

M&A, E&P, Capital Markets, Operations

Stacked Pays. Bone Spring & Wolfcamp

>32,000-Producing Wells.

~175-Rigs Running

2,186-Permits Issued Last 6 Months

660-DUCs Pending

4,900,000 Boepd: Gross Production

>$7 B in 1H2023 M&A, 22% of US Market

P/E Exits, Publics Buying

Includes List & Map of P/E and Private Cos.

DOWNLOAD 43 PAGE REPORT

STUDY 3001MA

Energy Advisors Group has released a review of the Delaware Basin as a continuation of our Market Monitor Series and thought leadership efforts. This 42-page Special Report provides unique perspectives on M&A, E&P and Capital Markets activity in the play. This report also includes a list and mapped positions of the remaining private and P/E backed companies as these targets dwindle in numbers by active acquisitions from the small and mid-cap publics.

Observations & Takeaways---

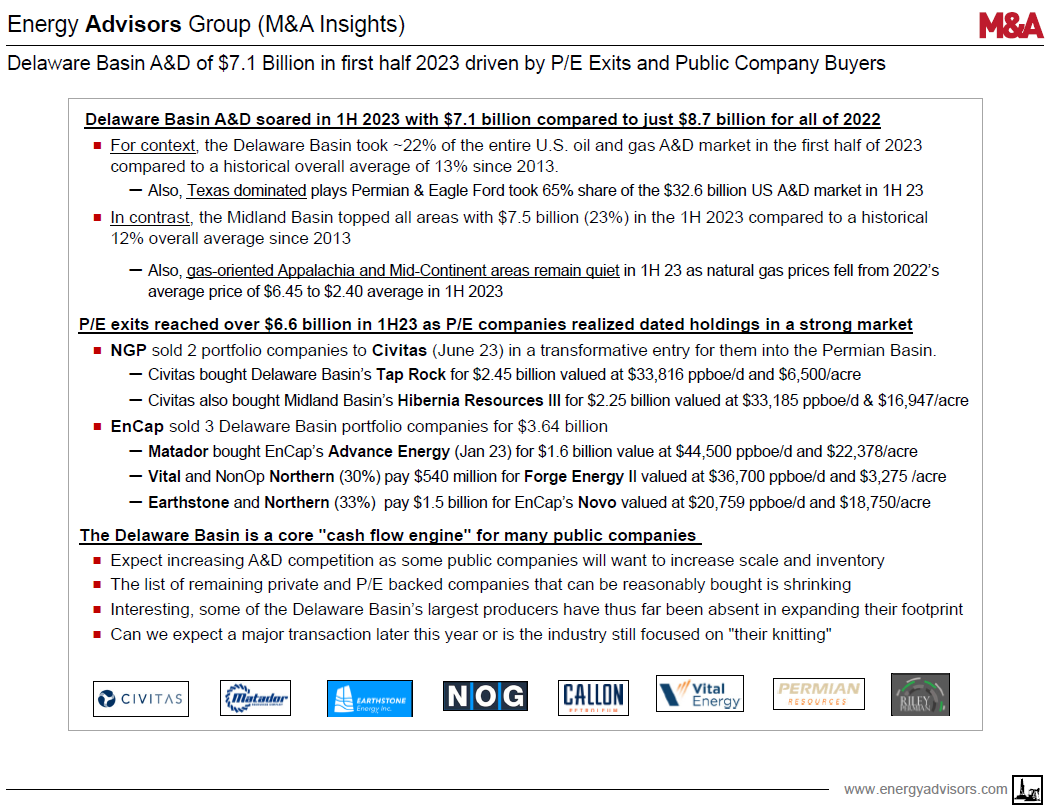

A&D - Soared to $7.1 Billion in 1H23

- Delaware Basin A&D soared in 1H 2023 to $7.1 billion – compared to just $8.7 billion in all of 2022

- Virtually 100% of the buyers were small to mid-cap publics increasing inventory and/or entering the Basin

- In Contrast, the sellers were highly dominated by P/E backed companies (93% of 1H 2023 deal value)

- Looking forward, there is a shrinking amount of private and P/E backed companies likely leading to increasing competition and/or an A&D market for public company mergers/acquisitions

- In numbers, EAG tallies 12 P/E backed companies and 24 private companies left that operate > 2,000 boe/d

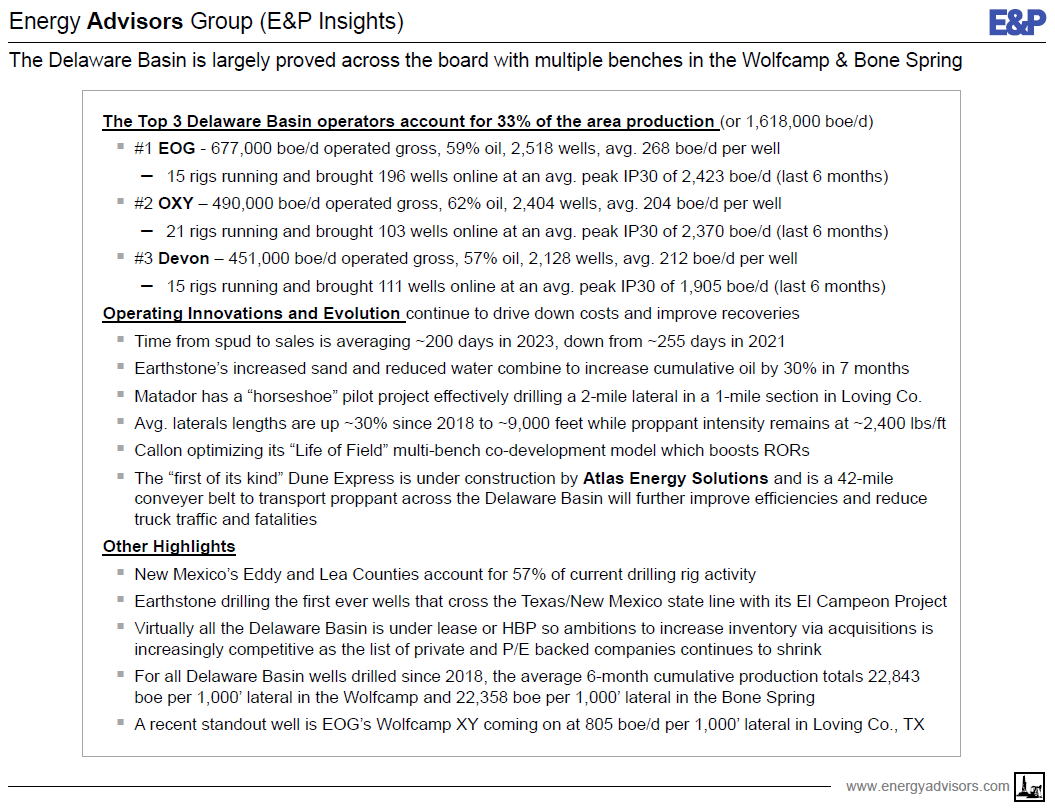

E&P - Simul Fracs, Horseshoe Well, Proppant Conveyer Belt

- Top 3 operators (EOG, Oxy, Devon) produced 1.62 MMboepd (33% of DB total) and running 51 rigs (29% of total)

- Lea and Eddy Counties, New Mexico have 57% share of the drilling rigs in Delaware Basin

- Operators continue to drive efficiencies and increase RORs through reduction in spud to sales time, use of simul fracs vs. zipper fracs, longer laterals, and focused multi-bench co-development field projects

- Matador has a “Horseshoe” pilot in Loving County which effectively drills a 2-mile lateral in a 1-mile section

- A “first of its kind” 42-mile conveyer belt for proppant transport is under construction by Atlas Energy Solutions – founded by Bud Brigham with a rare IPO on 03/09/23 – which will provide efficiencies and reduce truck fatalities

- Callon optimizing its multi-bench co-development “Life of Field” model to drive RORs higher

- Earthstone is drilling the first wells that cross the Texas/New Mexico state line with its El Campeon project

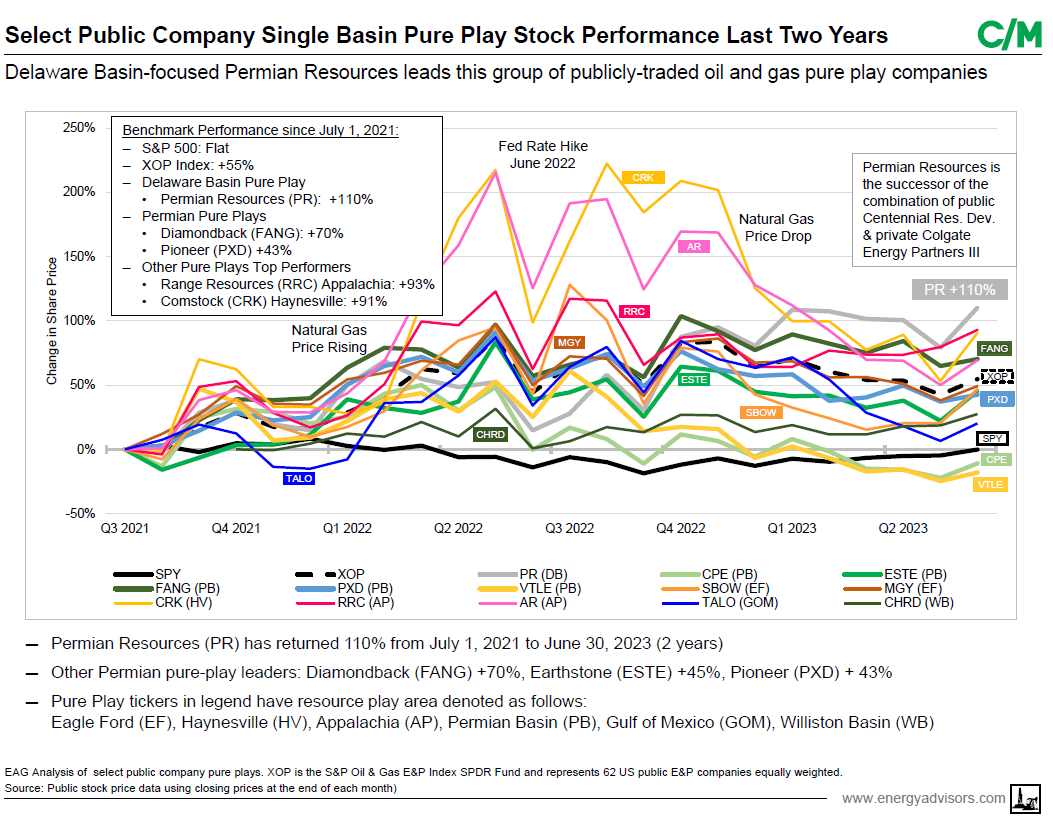

Capital Markets - P/E Exits, Permian Resources and Northern Oil & Gas Making Moves

- Delaware Basin pure play Permian Resources (+110% in past 2 years) is the star play far outperforming other resource pure play companies and 2x the XOP index (+55%)

- Private equity backed Delaware Basin companies hit the exit with $6.6 billion sold in 1H 2023 – mostly harvested by EnCap and NGP

- Interestingly, on the back of these exits, both EnCap and NGP are in the market after a multi-year hiatus raising new upstream funds (NGP targeting $4 billion, EnCap targeting $2.5 billion)

- Funding for the acquisitions is largely via increased RBLs with some capital market support via privately placed debt and also equity when accepted by the seller

- Non-Op Northern Oil & Gas stepped up and made a big move in 1H 2023 in two deals helping Earthstone and Vital Energy take down large acquisitions – structured as a % of undivided interest in the target and governed by a JOA

Operational Highlights - Earthstone Undergoing Rapid Growth

Our firm has also put together some slides on operational insights and looked at Earthstone as a firm undergoing rapid growth on the back of a disciplined A&D and Execution effort.

- Earthstone now has >700 operated wells in the Delaware and has the first wells to cross the Texas/New Mexico state line

- Permian Resources (result of Centennial and Colgate merger) is the largest pure-play Delaware Basin operator

- Matador is driving down D&C costs by ~10% to $1,041 per foot

- Devon is drilling 3-mile Wolfcamp laterals at its Exotic Cat Raider project in Lea County - top well 7,200 Boepd

- Callon's recent Percussion buy adds meaningful inventory with PV10 breakeven < $40 per bbl

Energy Advisors is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE

Energy Advisors Group

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

DELAWARE BASIN PERSPECTIVES

August 2, 2023; 42-Page Report

Delaware Basin

M&A, E&P, Capital Markets, Operations

Stacked Pays. Bone Spring & Wolfcamp

>32,000-Producing Wells.

~175-Rigs Running

2,186-Permits Issued Last 6 Months

660-DUCs Pending

4,900,000 Boepd: Gross Production

>$7 B in 1H2023 M&A, 22% of US Market

P/E Exits, Publics Buying

Includes List & Map of P/E and Private Cos.

DOWNLOAD 43 PAGE REPORT

STUDY 3001MA

Energy Advisors Group has released a review of the Delaware Basin as a continuation of our Market Monitor Series and thought leadership efforts. This 42-page Special Report provides unique perspectives on M&A, E&P and Capital Markets activity in the play. This report also includes a list and mapped positions of the remaining private and P/E backed companies as these targets dwindle in numbers by active acquisitions from the small and mid-cap publics.

Observations & Takeaways---

A&D - Soared to $7.1 Billion in 1H23

- Delaware Basin A&D soared in 1H 2023 to $7.1 billion – compared to just $8.7 billion in all of 2022

- Virtually 100% of the buyers were small to mid-cap publics increasing inventory and/or entering the Basin

- In Contrast, the sellers were highly dominated by P/E backed companies (93% of 1H 2023 deal value)

- Looking forward, there is a shrinking amount of private and P/E backed companies likely leading to increasing competition and/or an A&D market for public company mergers/acquisitions

- In numbers, EAG tallies 12 P/E backed companies and 24 private companies left that operate > 2,000 boe/d

E&P - Simul Fracs, Horseshoe Well, Proppant Conveyer Belt

- Top 3 operators (EOG, Oxy, Devon) produced 1.62 MMboepd (33% of DB total) and running 51 rigs (29% of total)

- Lea and Eddy Counties, New Mexico have 57% share of the drilling rigs in Delaware Basin

- Operators continue to drive efficiencies and increase RORs through reduction in spud to sales time, use of simul fracs vs. zipper fracs, longer laterals, and focused multi-bench co-development field projects

- Matador has a “Horseshoe” pilot in Loving County which effectively drills a 2-mile lateral in a 1-mile section

- A “first of its kind” 42-mile conveyer belt for proppant transport is under construction by Atlas Energy Solutions – founded by Bud Brigham with a rare IPO on 03/09/23 – which will provide efficiencies and reduce truck fatalities

- Callon optimizing its multi-bench co-development “Life of Field” model to drive RORs higher

- Earthstone is drilling the first wells that cross the Texas/New Mexico state line with its El Campeon project

Capital Markets - P/E Exits, Permian Resources and Northern Oil & Gas Making Moves

- Delaware Basin pure play Permian Resources (+110% in past 2 years) is the star play far outperforming other resource pure play companies and 2x the XOP index (+55%)

- Private equity backed Delaware Basin companies hit the exit with $6.6 billion sold in 1H 2023 – mostly harvested by EnCap and NGP

- Interestingly, on the back of these exits, both EnCap and NGP are in the market after a multi-year hiatus raising new upstream funds (NGP targeting $4 billion, EnCap targeting $2.5 billion)

- Funding for the acquisitions is largely via increased RBLs with some capital market support via privately placed debt and also equity when accepted by the seller

- Non-Op Northern Oil & Gas stepped up and made a big move in 1H 2023 in two deals helping Earthstone and Vital Energy take down large acquisitions – structured as a % of undivided interest in the target and governed by a JOA

Operational Highlights - Earthstone Undergoing Rapid Growth

Our firm has also put together some slides on operational insights and looked at Earthstone as a firm undergoing rapid growth on the back of a disciplined A&D and Execution effort.

- Earthstone now has >700 operated wells in the Delaware and has the first wells to cross the Texas/New Mexico state line

- Permian Resources (result of Centennial and Colgate merger) is the largest pure-play Delaware Basin operator

- Matador is driving down D&C costs by ~10% to $1,041 per foot

- Devon is drilling 3-mile Wolfcamp laterals at its Exotic Cat Raider project in Lea County - top well 7,200 Boepd

- Callon's recent Percussion buy adds meaningful inventory with PV10 breakeven < $40 per bbl

Energy Advisors is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE

Energy Advisors Group

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123