03Q23 QUARTERLY M&A REPORT

Research

All Standard Disclaimers Apply & Seller Rights Retained

DEAL PERSPECTIVES (MEDIA VERSION)

34-Page Report

U.S. A&D Review and Themes - 3Q 2023

$14.1 Billion in Deals, Down 42%

All Top 10 Deals Are Oil-Weighted

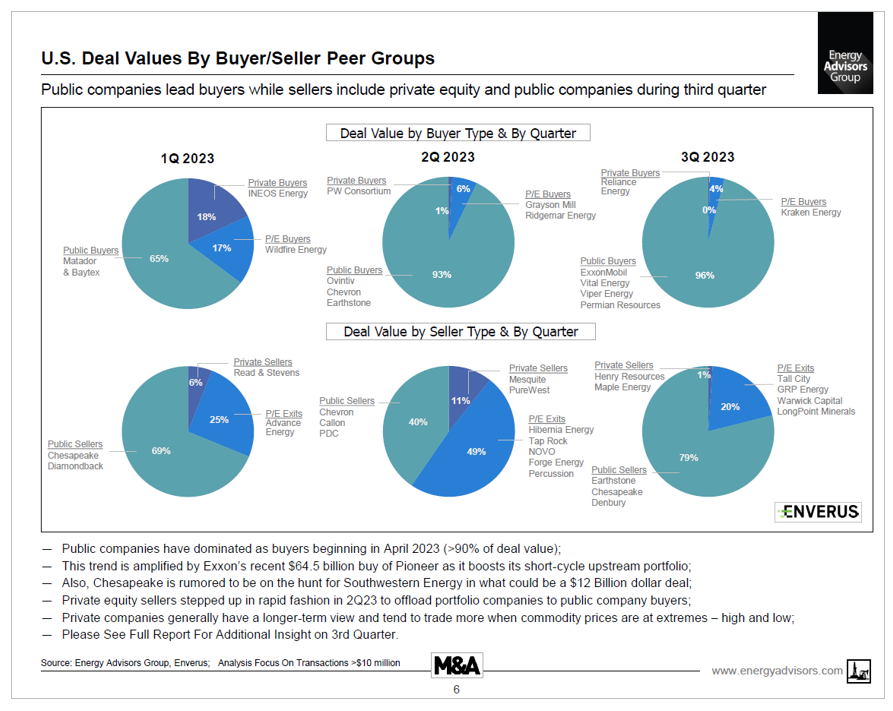

Public Companies Buy 96% of Deals

Permian Basin Remains Hotspot

Expect Publics to Continue Buying

Look for Return of Natural Gas Deals

Small to Mid Size Deals to Increase

New Smaller Private Equity Players Entering

Valuations Reflect Higher Interest Rates

XOM Buys Denbury in Largest Deal - $4.9 Bn

After Q3, XOM Also Buys PXD - $64.5 Bn

CONTACT EAG FOR FULL 34 PAGE REPORT

STUDY 6001MA

Energy Advisors Group has released a Q3 2023 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. This 34-page Special Report provides perspectives on past and current trends in deal values, counts, plays and valuations. Also included are important forward looking themes as buyers and sellers look to navigate a plethora of dynamics of the capital markets and interest rates, oil and gas supply and demand, regulatory and energy transition impacts, play economics and technology, and geopolitical risks.

Energy Advisors Group has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side.

Takeaways from 3Q 2023 are:

- Not counting XOM/PXD, there was $14.1 Bn in deals reported by Enverus in 3Q 2023 down 42% from $24.3 Bn 2Q 2023;

- Current average production multiples are ~$37,000 ppbo/d for oil and ~$2,475 ppmcf/d for natural gas;

- EBITDA multiples are clustering around 3x forward 12-month forecasts;

- Four transactions greater than $1 Bn in 3Q 2023; compared to six in the prior quarter and four in 1Q 2023;

- All Top 10 deals in 3Q 2023 were oil-weighted and all buyers were publics, often using equity as currency;

- After a surge of PE sellers representing ~50% of 2Q 2023 deal value, the seller landscape reverts to a more normal pace with public companies taking a 79% share of deal value on the sell side;

- ExxonMobil’s $4.9 Bn equity purchase of Denbury Resources was done at only a slight 2% premium; the acquisition furthers the super majors’ desire to accelerate its low carbon solutions business;

- The Permian continues to be hot with $5.8 Bn in deals in 3Q 2023 lead by Delaware Basin pure-play Permian Resources equity purchase (plus debt) purchase of Earthstone Resources for $4.5 Bn stuck at a 15% premium to Earthstone’s stock price prior to deal announcement;

- Outside of the Permian, the Eagle Ford and Bakken witnessed transactions consistent with 2Q 2023 volumes;

- Viper strikes the third largest recorded royalty buy w/ a $1.0 Bn purchase (90% Permian) of private-equity players GRP Energy Capital & Warwick Capital Group;

- Chesapeake completes its exit from the Eagle Ford with a final $700 million sale to SilverBow – bringing its tally for its Eagle Ford assets to >$3.5 Bn - the OKC independent now turns its gas-pivot to the Haynesville and Marcellus with press time rumors of its interest in acquiring Southwestern;

- Vital Energy (formerly Laredo Petroleum) remains on a hot streak doing three more deals for $1.2 Bn on the heels of its $216 million transaction in 1Q 2023 and $378 million in 2Q 2023;

- Gas-oriented transactions remain quiet as gas prices continue nursing the price downdraft from 2022’s quarterly spike of $6.45/MMBtu;

- Enverus reports $47 Bn in deals YTD compared to $58 Bn in 2022 and $67 Bn in 2021;

- Average deal size YTD has nearly doubled to $923 million versus $505 million in 2022 and $541 million in 2021 says the Austin boys.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE REPORT CONTACT:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

DEAL PERSPECTIVES (MEDIA VERSION)

34-Page Report

U.S. A&D Review and Themes - 3Q 2023

$14.1 Billion in Deals, Down 42%

All Top 10 Deals Are Oil-Weighted

Public Companies Buy 96% of Deals

Permian Basin Remains Hotspot

Expect Publics to Continue Buying

Look for Return of Natural Gas Deals

Small to Mid Size Deals to Increase

New Smaller Private Equity Players Entering

Valuations Reflect Higher Interest Rates

XOM Buys Denbury in Largest Deal - $4.9 Bn

After Q3, XOM Also Buys PXD - $64.5 Bn

CONTACT EAG FOR FULL 34 PAGE REPORT

STUDY 6001MA

Energy Advisors Group has released a Q3 2023 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. This 34-page Special Report provides perspectives on past and current trends in deal values, counts, plays and valuations. Also included are important forward looking themes as buyers and sellers look to navigate a plethora of dynamics of the capital markets and interest rates, oil and gas supply and demand, regulatory and energy transition impacts, play economics and technology, and geopolitical risks.

Energy Advisors Group has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side.

Takeaways from 3Q 2023 are:

- Not counting XOM/PXD, there was $14.1 Bn in deals reported by Enverus in 3Q 2023 down 42% from $24.3 Bn 2Q 2023;

- Current average production multiples are ~$37,000 ppbo/d for oil and ~$2,475 ppmcf/d for natural gas;

- EBITDA multiples are clustering around 3x forward 12-month forecasts;

- Four transactions greater than $1 Bn in 3Q 2023; compared to six in the prior quarter and four in 1Q 2023;

- All Top 10 deals in 3Q 2023 were oil-weighted and all buyers were publics, often using equity as currency;

- After a surge of PE sellers representing ~50% of 2Q 2023 deal value, the seller landscape reverts to a more normal pace with public companies taking a 79% share of deal value on the sell side;

- ExxonMobil’s $4.9 Bn equity purchase of Denbury Resources was done at only a slight 2% premium; the acquisition furthers the super majors’ desire to accelerate its low carbon solutions business;

- The Permian continues to be hot with $5.8 Bn in deals in 3Q 2023 lead by Delaware Basin pure-play Permian Resources equity purchase (plus debt) purchase of Earthstone Resources for $4.5 Bn stuck at a 15% premium to Earthstone’s stock price prior to deal announcement;

- Outside of the Permian, the Eagle Ford and Bakken witnessed transactions consistent with 2Q 2023 volumes;

- Viper strikes the third largest recorded royalty buy w/ a $1.0 Bn purchase (90% Permian) of private-equity players GRP Energy Capital & Warwick Capital Group;

- Chesapeake completes its exit from the Eagle Ford with a final $700 million sale to SilverBow – bringing its tally for its Eagle Ford assets to >$3.5 Bn - the OKC independent now turns its gas-pivot to the Haynesville and Marcellus with press time rumors of its interest in acquiring Southwestern;

- Vital Energy (formerly Laredo Petroleum) remains on a hot streak doing three more deals for $1.2 Bn on the heels of its $216 million transaction in 1Q 2023 and $378 million in 2Q 2023;

- Gas-oriented transactions remain quiet as gas prices continue nursing the price downdraft from 2022’s quarterly spike of $6.45/MMBtu;

- Enverus reports $47 Bn in deals YTD compared to $58 Bn in 2022 and $67 Bn in 2021;

- Average deal size YTD has nearly doubled to $923 million versus $505 million in 2022 and $541 million in 2021 says the Austin boys.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE REPORT CONTACT:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123