MARCELLUS/UTICA REGION STUDY V2

Research

All Standard Disclaimers Apply & Seller Rights Retained

APPALACHIAN BASIN PERSPECTIVES V2

April 22, 2025. 51-Page Report.

APPALACHIAN BASIN

MARCELLUS & UTICA

M&A, E&P, Capital Markets, Midstream

34.1 Bcfpd and 148,000 Bopd

~34-Rigs Running, 782-Wells Online 2024

Basin Constrained by Takeaway

Low Cost Structures Bode Well in Higher Gas

EQT, EXPAND, ANTERO Top 3 Producers

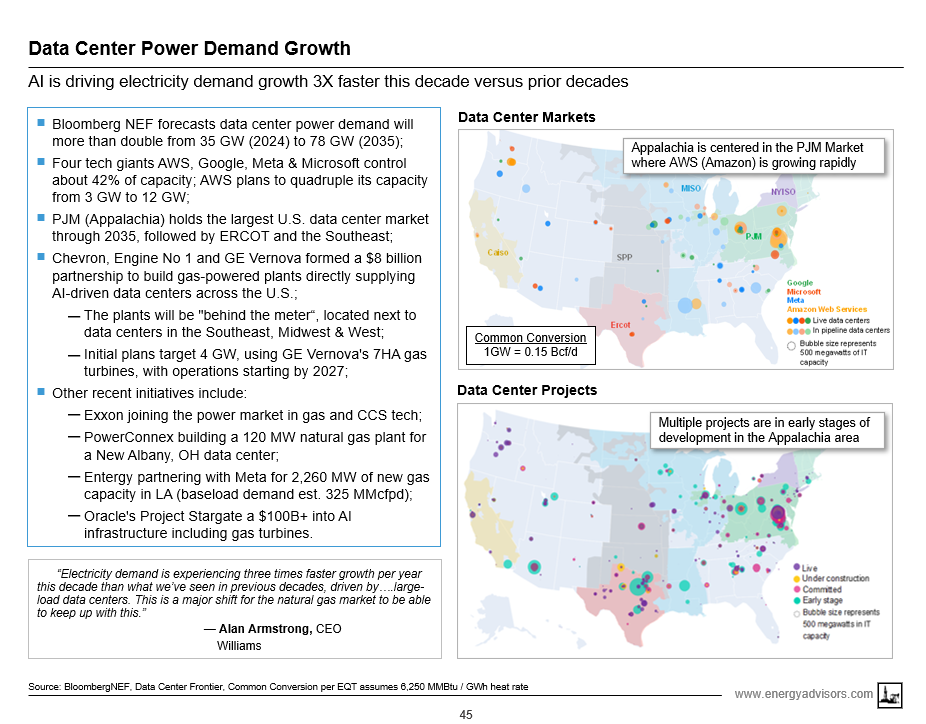

Power Gen and LNG Driving Demand Growth

Challenges In Takeaway Persist Short Term

Utica Oil Setting Records, Mainly E. Ohio

Large P/E Backed Operators May IPO/Sell

Infinity Natural Resources Goes Public

DOWNLOAD 51 PAGE REPORT

STUDY 4003MA

Energy Advisors Group has released Volume 2 of our Appalachian Basin Study as a continuation of our Market Monitor Series and thought leadership efforts. This 51-page Special Report provides unique perspectives on M&A, E&P Capital Markets, Demand Factors, and Midstream Activity in the play. The report also includes a list of the Top private, P/E backed, and public companies with production and activity stats.

Here are our quick quotes and takeaways from our report.

Quick Quotes:

------- Strategic. “The Appalachian Basin is the nation’s largest natural gas play and has the resources to meet growing natural gas demands, but is constrained by takeaway. Operators are stepping up to the challenge and reducing costs.”

------- Higher Natural Gas Prices. "Appalachia is home to some of the world’s largest gas players and they are ready to meet the call for more natural gas, they have fine-tuned their businesses to prosper at today’s pricing and should do very well at even higher pricing."

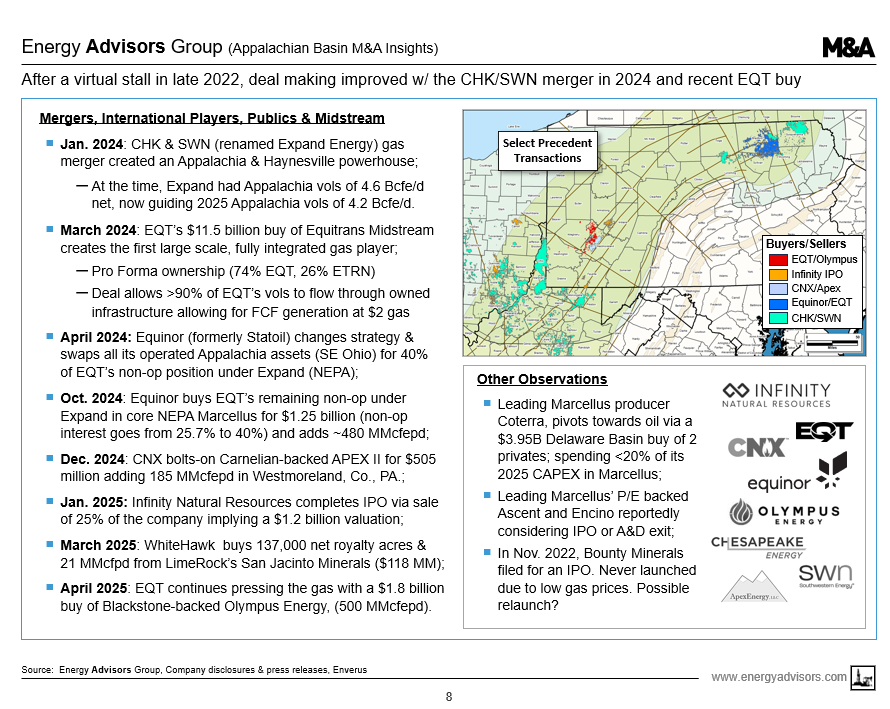

-------Attractive A&D. "We expect M&A activity in Appalachia to increase as scale matters. EQT just inked a $1.8 billion buy of Olympus at 3.4x adj. EBITDA and ~15% unlevered FCF yield and Blackstone took 72% of the proceeds in EQT equity - a signal that Blackstone sees further upside in EQT equity."

-------Expect More A&D. "As gas recovers, firms like Ascent and Encino are considering sales via A&D exit or IPO."

-------Low Cost Structures. "Equinor's material non-op under EXPAND is well-positioned in premium acreage with low-breakevens. EQT's vertically integrated position allows for long term FCF at $2.00 gas."

-------Midstream? "Mountain Valley Pipeline (2 Bcfpd) online in 2Q24 taking gas southbound to Transco Station 165 in Virginia and Transco Regional Energy Access compression upgrade in 4Q24 added 830,000 MMcfpd capacity to New Jersey and Pennsylvania. Further material projects not expected until late 2027. William's Constitution Pipeline (canceled in 2020) in news again as Feds want more gas flows towards New York but NY Governor faces environmental opposition."

------LNG and Data Center Power Gen! "As Gulf Coast LNG projects come online, Appalachia gas will be needed to backfill demand in the NE & Midwest. Power for Data Centers need all-of-the-above strategy with Appalachia gas attractive in areas like Pittsburgh industrial corridor. Long term agreements require operators to be investment grade credits."

------Innovation! "EQT's vertical business model allows for pressure reduction projects that are outperforming expectations by 2X - three pilot sites showed a 3.1- 3.5 Bcf uplift in Year 1."

Observations & Takeaways---

A&D – Upstream Totaled $1.4 Billion in 2024 (excluding EQT buy of ETRN Midstream & CHK/SWN merger)

- 2024 Appalachia upstream deal flow remained slow with just 3 A&D deals done in 2024, same as 2023;

- Midstream - EQT bought Equitrans Midstream for $11.6 billion to become major vertically integrated gas company;

- CHK merged with SWN (Appalachia and Haynesville) and rebranded as Expand Energy;

- Infinity Natural Resources IPO (P/E backed by NGP, Pearl) in Jan. 2025 sold 25% and valued INR at $1.2 B;

- EQT pressed the gas pedal again in April 2025 buying P/E backed Olympus Energy for $1.8 billion;

- Expect increased A&D as gas prices recover and P/E backed firms like Ascent, Encino considering exit or IPO.

E&P – Horizontal Redevelopment, Vertical Gas, Emerging Plays, EOR

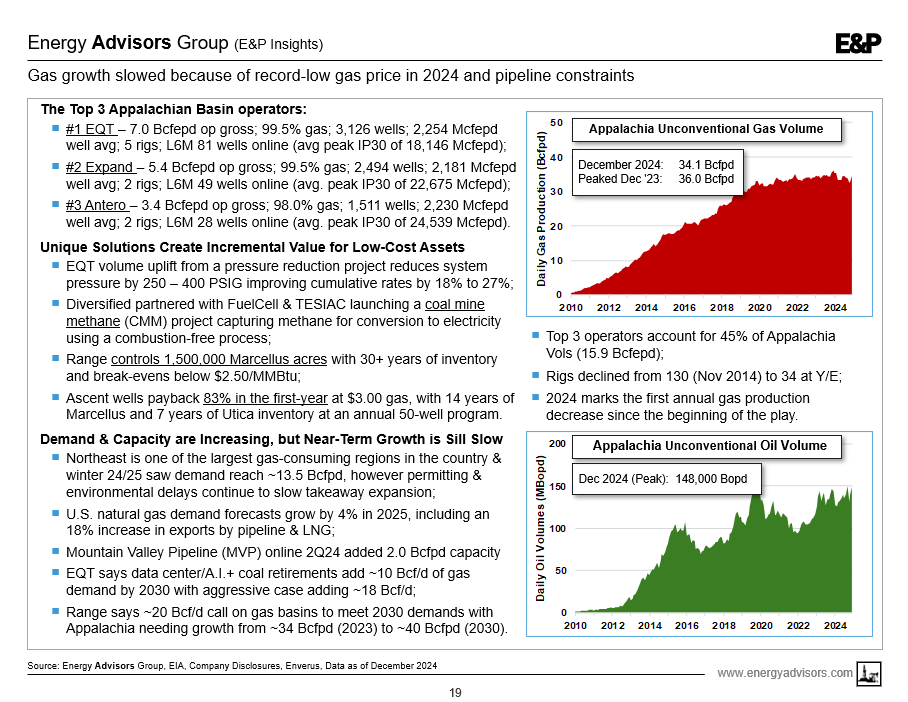

- HZ Volumes of ~34.1 Bcfpd and 148,000 Bopd (December 2024) with 34 horizontal rigs running;

- Conventional volumes of ~1 Bcfepd (~97% natural gas);

- Activity has seen 21,135 hz wells online since 2010, 4,926 since 2020; Lateral lengths up 50% since 2018 (now ~13,000’);

- Top 6 Operators are EQT (7.1 Bcfepd), Expand (5.4), Antero (3.4), Coterra (2.8); Ascent (2.5), Range (2.2);

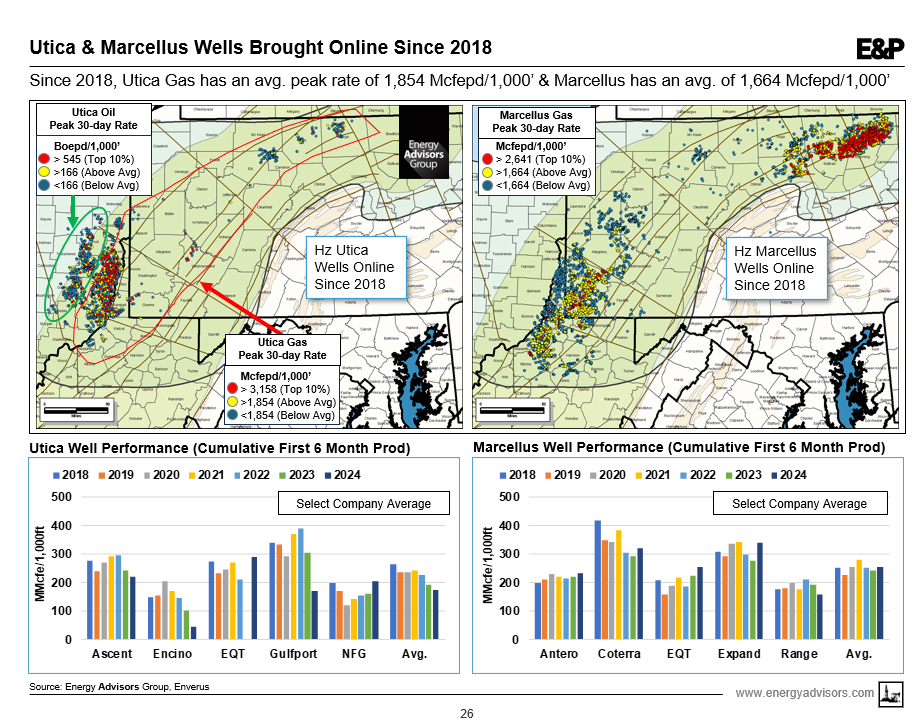

- Wells see avg. IP30/1,000’ since 2018 in Marcellus Gas (1.6 MMcfepd), Utica Gas (1.8 MMcfepd), Utica Oil (166 Boepd);

- Utica oil setting records as EOG is developing a oil/liquids play in eastern Ohio;

Midstream & Demand – Appalachia is Pipe Constrained in Short Term but Benefits from Higher Gas Prices

- Takeaway capacity from Basin constrained in short term but call on Appalachia gas will be needed to backfill Northeast and Midwest markets as more U.S. gas heads to Gulf Coast amid rising LNG exports;

- LNG and AI/Power Gen will require 20 Bcfpd+ of US gas by 2030;

- In Basin Gas can support Data Center buildout in areas like the industrial corridor of Pittsburgh.

Capital Markets – Appalachia Publics Stocks Outperforming, an IPO & P/E Privates Looking to Get Liquid

- Last 2 years, pure plays AR (+76%), EQT (+53%), RRC (+51%) outperform XOP (+4%) AND S&P 500 (+34%);

- Gas prices up: Demand + winter storage draw (+21% vs. 5-yr avg) drove gas strip +43% YoY ($3.92/$2.75 as of April 15);

- IPO :Infinity Natural Resources (Utica oil and Appalachia gas optionality) succeeds in going public;

- More to come: P/E funded Ascent, Encino, Greylock all reportedly open to exit; Ascent, Encino, Bounty Minerals may IPO.

-- Here is a page that provides a quick recap and timeline of deals beginning with the CHK/SWN merger

-- We included this slide to show Appalachia vols since 2010 along with Top 3 operators (45% of these vols)

-- Our third slide here shows and classifies all wells online since 2018 for Marcellus gas, Utica gas and Utica oil

-- Our last slide here helps get your arms around data centers (where, who, size) - Amazon is key to Appalachia

Energy Advisors is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE:

Energy Advisors Group

Blake Dornak

Vice President

Phone: 713-600-0169

---Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

APPALACHIAN BASIN PERSPECTIVES V2

April 22, 2025. 51-Page Report.

APPALACHIAN BASIN

MARCELLUS & UTICA

M&A, E&P, Capital Markets, Midstream

34.1 Bcfpd and 148,000 Bopd

~34-Rigs Running, 782-Wells Online 2024

Basin Constrained by Takeaway

Low Cost Structures Bode Well in Higher Gas

EQT, EXPAND, ANTERO Top 3 Producers

Power Gen and LNG Driving Demand Growth

Challenges In Takeaway Persist Short Term

Utica Oil Setting Records, Mainly E. Ohio

Large P/E Backed Operators May IPO/Sell

Infinity Natural Resources Goes Public

DOWNLOAD 51 PAGE REPORT

STUDY 4003MA

Energy Advisors Group has released Volume 2 of our Appalachian Basin Study as a continuation of our Market Monitor Series and thought leadership efforts. This 51-page Special Report provides unique perspectives on M&A, E&P Capital Markets, Demand Factors, and Midstream Activity in the play. The report also includes a list of the Top private, P/E backed, and public companies with production and activity stats.

Here are our quick quotes and takeaways from our report.

Quick Quotes:

------- Strategic. “The Appalachian Basin is the nation’s largest natural gas play and has the resources to meet growing natural gas demands, but is constrained by takeaway. Operators are stepping up to the challenge and reducing costs.”

------- Higher Natural Gas Prices. "Appalachia is home to some of the world’s largest gas players and they are ready to meet the call for more natural gas, they have fine-tuned their businesses to prosper at today’s pricing and should do very well at even higher pricing."

-------Attractive A&D. "We expect M&A activity in Appalachia to increase as scale matters. EQT just inked a $1.8 billion buy of Olympus at 3.4x adj. EBITDA and ~15% unlevered FCF yield and Blackstone took 72% of the proceeds in EQT equity - a signal that Blackstone sees further upside in EQT equity."

-------Expect More A&D. "As gas recovers, firms like Ascent and Encino are considering sales via A&D exit or IPO."

-------Low Cost Structures. "Equinor's material non-op under EXPAND is well-positioned in premium acreage with low-breakevens. EQT's vertically integrated position allows for long term FCF at $2.00 gas."

-------Midstream? "Mountain Valley Pipeline (2 Bcfpd) online in 2Q24 taking gas southbound to Transco Station 165 in Virginia and Transco Regional Energy Access compression upgrade in 4Q24 added 830,000 MMcfpd capacity to New Jersey and Pennsylvania. Further material projects not expected until late 2027. William's Constitution Pipeline (canceled in 2020) in news again as Feds want more gas flows towards New York but NY Governor faces environmental opposition."

------LNG and Data Center Power Gen! "As Gulf Coast LNG projects come online, Appalachia gas will be needed to backfill demand in the NE & Midwest. Power for Data Centers need all-of-the-above strategy with Appalachia gas attractive in areas like Pittsburgh industrial corridor. Long term agreements require operators to be investment grade credits."

------Innovation! "EQT's vertical business model allows for pressure reduction projects that are outperforming expectations by 2X - three pilot sites showed a 3.1- 3.5 Bcf uplift in Year 1."

Observations & Takeaways---

A&D – Upstream Totaled $1.4 Billion in 2024 (excluding EQT buy of ETRN Midstream & CHK/SWN merger)

- 2024 Appalachia upstream deal flow remained slow with just 3 A&D deals done in 2024, same as 2023;

- Midstream - EQT bought Equitrans Midstream for $11.6 billion to become major vertically integrated gas company;

- CHK merged with SWN (Appalachia and Haynesville) and rebranded as Expand Energy;

- Infinity Natural Resources IPO (P/E backed by NGP, Pearl) in Jan. 2025 sold 25% and valued INR at $1.2 B;

- EQT pressed the gas pedal again in April 2025 buying P/E backed Olympus Energy for $1.8 billion;

- Expect increased A&D as gas prices recover and P/E backed firms like Ascent, Encino considering exit or IPO.

E&P – Horizontal Redevelopment, Vertical Gas, Emerging Plays, EOR

- HZ Volumes of ~34.1 Bcfpd and 148,000 Bopd (December 2024) with 34 horizontal rigs running;

- Conventional volumes of ~1 Bcfepd (~97% natural gas);

- Activity has seen 21,135 hz wells online since 2010, 4,926 since 2020; Lateral lengths up 50% since 2018 (now ~13,000’);

- Top 6 Operators are EQT (7.1 Bcfepd), Expand (5.4), Antero (3.4), Coterra (2.8); Ascent (2.5), Range (2.2);

- Wells see avg. IP30/1,000’ since 2018 in Marcellus Gas (1.6 MMcfepd), Utica Gas (1.8 MMcfepd), Utica Oil (166 Boepd);

- Utica oil setting records as EOG is developing a oil/liquids play in eastern Ohio;

Midstream & Demand – Appalachia is Pipe Constrained in Short Term but Benefits from Higher Gas Prices

- Takeaway capacity from Basin constrained in short term but call on Appalachia gas will be needed to backfill Northeast and Midwest markets as more U.S. gas heads to Gulf Coast amid rising LNG exports;

- LNG and AI/Power Gen will require 20 Bcfpd+ of US gas by 2030;

- In Basin Gas can support Data Center buildout in areas like the industrial corridor of Pittsburgh.

Capital Markets – Appalachia Publics Stocks Outperforming, an IPO & P/E Privates Looking to Get Liquid

- Last 2 years, pure plays AR (+76%), EQT (+53%), RRC (+51%) outperform XOP (+4%) AND S&P 500 (+34%);

- Gas prices up: Demand + winter storage draw (+21% vs. 5-yr avg) drove gas strip +43% YoY ($3.92/$2.75 as of April 15);

- IPO :Infinity Natural Resources (Utica oil and Appalachia gas optionality) succeeds in going public;

- More to come: P/E funded Ascent, Encino, Greylock all reportedly open to exit; Ascent, Encino, Bounty Minerals may IPO.

-- Here is a page that provides a quick recap and timeline of deals beginning with the CHK/SWN merger

-- We included this slide to show Appalachia vols since 2010 along with Top 3 operators (45% of these vols)

-- Our third slide here shows and classifies all wells online since 2018 for Marcellus gas, Utica gas and Utica oil

-- Our last slide here helps get your arms around data centers (where, who, size) - Amazon is key to Appalachia

Energy Advisors is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE:

Energy Advisors Group

Blake Dornak

Vice President

Phone: 713-600-0169

---Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123